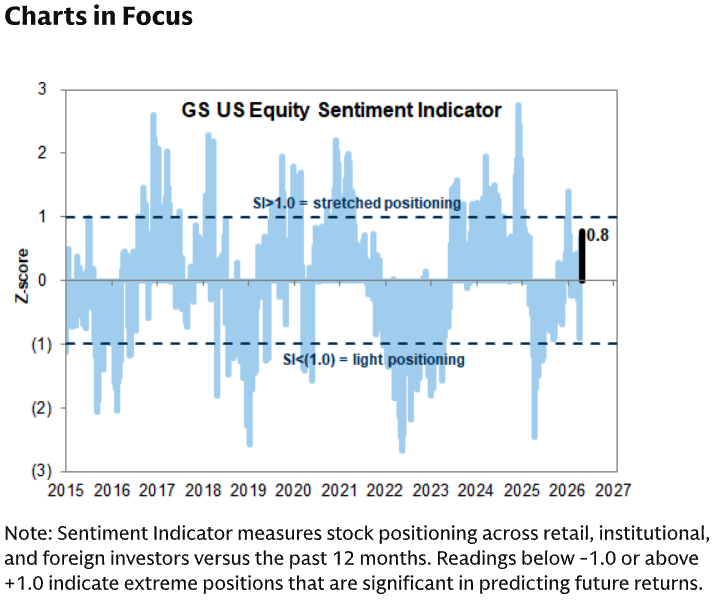

Institutional Insights: Goldman Sachs SP500 Positioning & Key Levels 21/4/26

Positioning remains supportive for equities, with systematic demand still strong, prime books adding selectively, and buyback support set to improve as blackout windows roll off.

CTA / systematic flows

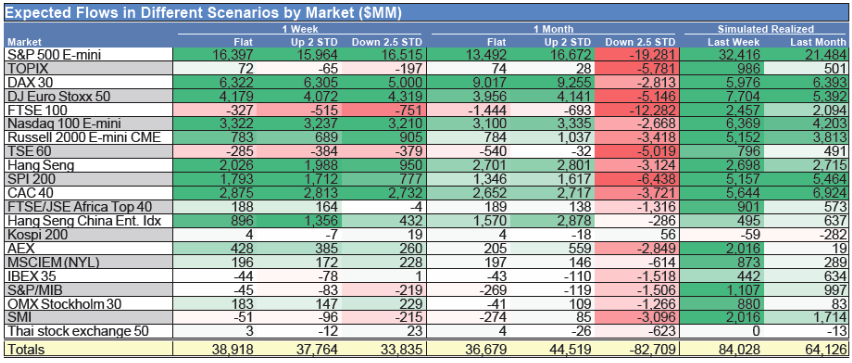

CTA signals remain supportive near term. Over the next week, model estimates suggest continued buying in all scenarios: roughly $39bn in a flat tape, $38bn in an up tape, and $34bn even in a down tape. US equities account for around $20bn of that demand across all three outcomes, implying that systematic support should remain a tailwind in the very near term.

The picture becomes more conditional over the next month. In flat and up markets, CTAs are still expected to be net buyers, with projected demand of $37bn and $45bn, respectively. But in a down tape, that support flips decisively, with models implying roughly $83bn of global selling, including around $25bn out of US equities.

For the S&P 500, the key pivot levels to watch are 6,787 in the short term, 6,761 on a medium-term basis, and 6,412 over the longer term. As long as spot remains above those thresholds, the systematic flow backdrop should stay broadly constructive; a sustained break lower would materially raise the risk of CTA selling pressure building.

Prime brokerage / hedge fund positioning

GS prime data point to a constructive but selective risk-add. Global equities were net bought for a second straight week, driven entirely by long buying, with Europe and EM Asia leading. Macro products were bought for a third consecutive week, while single stocks were broadly flat.

The clearest concentration remains in TMT and EM Asia. Information Technology, Communication Services, and Health Care were the largest net buys globally, while global TMT exposure has risen to five-year highs. EM Asia was also among the strongest net-buy regions, with both gross and net exposures now near the top of historical ranges.

By contrast, US equities were modest net sold, with short sales outpacing long buys. Within the US, Financials were a notable bright spot, seeing their first net buying in 11 weeks and at the fastest pace year-to-date, driven mainly by short covering. Industrials went the other way, with hedge funds selling the sector at the fastest pace in five weeks; the group has now been net sold in 10 of the last 12 weeks, leaving positioning close to the bottom of the one-year range.

Leverage and book backdrop

At the portfolio level, gross leverage remains elevated, while net leverage is still relatively subdued, suggesting investors are adding exposure but not aggressively. That fits the broader picture of a market where risk appetite has improved, but where positioning is still far from euphoric outside a few crowded themes.

Buybacks

Buyback support remains light for now, with many corporates still in blackout. Goldman estimates only ~18% of companies are currently in open window, but that should rise to ~29% by the end of the week as earnings reports come through. Recent buyback flow has been relatively modest, though skewed toward Communication Services, Financials, and Consumer Discretionary.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!